An interest rate swap is an agreement between two parties to exchange fixed and floating interest payments with each other over a specified period of time. At the time of the swap agreement, the total value of the fixed rate flows of the swap equals the value of the expected floating interest payments. This causes the value of the swap to change in relation to the expected future level of interest rates.

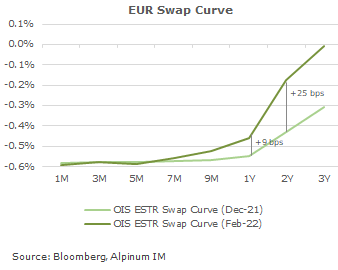

Rising inflation figures and a subsequent hawkish tone from the ECB opens up the likelihood of an earlier rate hike, leading to a steepening of the swap yield curve for the short tenors. This caused the European short-term credit market into flux: The ICE BofA 1-3 Year Euro Corporate Index lost over 1% in February.