Elevated income buffers adverse market development

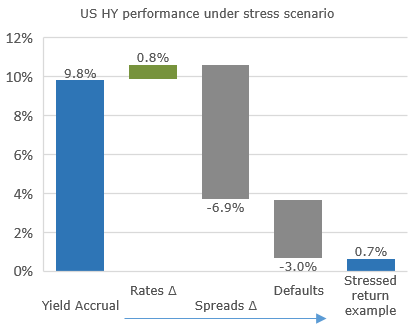

With yields at almost 10% p.a., US HY offers investors a very solid buffer during adverse market development. This can be illustrated by a hypothetical multi-factor 12-month scenario, stressing the projected total return with a simultaneous risk-free rate curve steepening (-25bps on short and +100bps on long maturities), credit spreads widening (+200bps) and elevated realized […]

Elevated income buffers adverse market development Read More »